A healthcare construction boom in expected over the next two years, bolstered by Government capital investment and the sector’s high profile over the past 18 months.

According to Glenigan’s UK Construction Industry Forecast 2022-2023 report, published earlier this month, the outlook for the healthcare construction industry remains bright, with a 3.8% real-term growth rate in NHS capital funding set to lift project starts over the forecast period.

This is supported by the Government’s £4.2bn increase in health capital announced in the last Spending Review.

And it comes hot on the heels of previously-announced plans to build 40 new hospitals by 2030 and upgrade more than 70 others over the same period.

But the report, authored by Glenigan’s economics director, Allan Wilen; and senior economist, Rhys Gadsby, warns it may take time for some of the new projects to get to the site.

“The Nightingale temporary hospital programme added a significant boost to health sector project starts in 2020, which grew by a total of 37% against 2019 performance,” the report reveals.

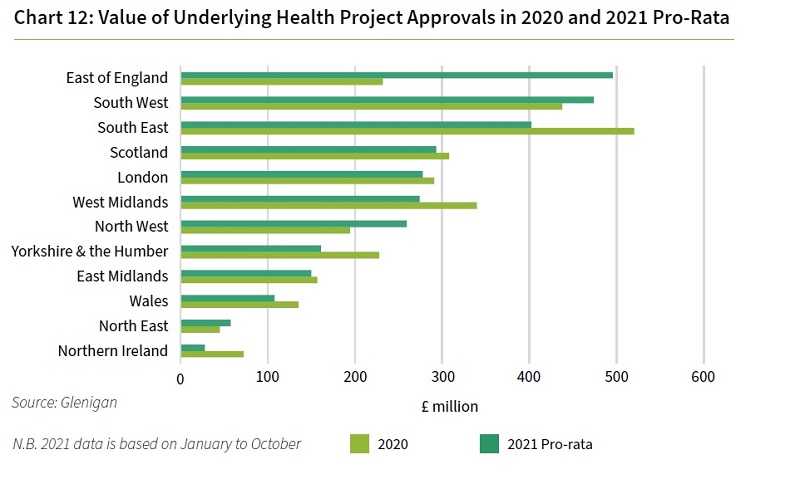

The value of underlying health project planning approvals is growing in a number of geographical areas, including the East, North West, and South West of England

“And, although the value is projected to slip back by 7% in 2021, project starts are anticipated to remain very high compared with pre-pandemic levels.”

The value of health detailed planning approvals fell 7% in 2018, the report states, following a strong performance during the previous year.

Encouragingly, though, health project approvals have increased since then, with rises of 3% in 2019 and 32% in 2020.

And approvals remained high during 2021 to October, rising 9% against the previous year.

“The additional government funding promised in the Spending Review should feed through to sector activity towards the end of the forecast period,” the report states.

“Project starts are forecast to fall slightly during 2021, but remain high compared with any year prior to the pandemic.

“And we expect project starts to increase 5% in 2022 and 4% in 2023 as new projects come forward and as NHS trusts develop and implement their investment programmes.

The health sector is set to see growth in the value of underlying project starts of 5% and 4% in 2022/23, according to the report

“By the end of the forecast period, we expect project starts to surpass the strong performance experienced in 2020.”

The health and civil engineering sectors have both seen additional funding over recent months, and are helping the construction sector to recover from both COVID-19 and the knock-on effect of Brexit.

The report states that, across the majority of sectors, construction activity has moderated due, in part, to material and labour supply issues.

“Post-Brexit customs regulations and non-tariff barriers continue to disrupt supply chains both for the construction industry and across the wider UK economy,” it adds.

“Brexit and the pandemic have also intensified the labour shortages, both in construction and supporting industries such as logistics.

“And this is expected to disrupt the economic recovery from the pandemic.”

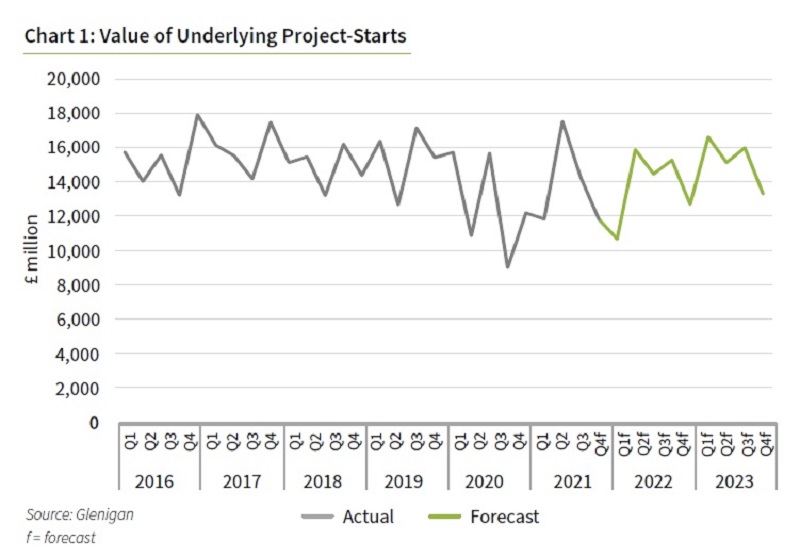

Across all sectors, construction activity recovered strongly during the first quarter of 2021 as the vaccine rollout and progressive unlocking of the economy started to rebuild confidence and as contractors started pandemic-delayed projects.

However, after this sharp initial surge of delayed projects, the flow of work has moderated during the rest of 2021, due in part to material supply disruptions.

Nevertheless, starts remain substantially ahead of last year.

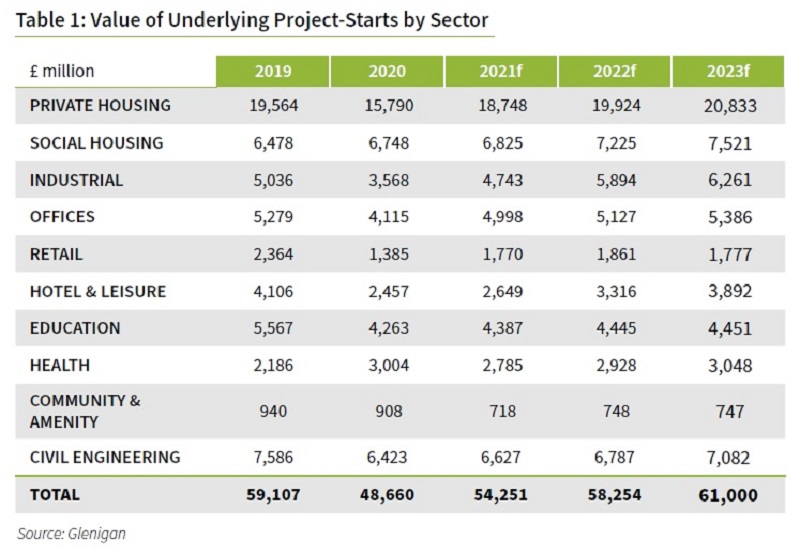

This table shows the value of underlying project starts across all construction sectors

At £54.2bn, the value of underlying starts (projects with a construction value of less than £100m) during 2021 is expected to be 11% up on last year, although 8% behind pre-pandemic levels seen in 2019.

“The recovery will be driven by strong growth in health and industrial projects, increases in private and social residential activity, and a belated recovery in the hotel and leisure sector,” says the report.

“And, regionally, growth will be strongest across the Midlands and the North of England, as the Government’s ‘levelling-up’ agenda provides a spur to new development activity.

“Wales, Scotland and Northern Ireland are also forecast to outpace overall UK growth.”